When Should Board of Directors Composition Be Finalised for an IPO in India

Board composition should be IPO-ready 12–18 months before a targeted listing date – not during DRHP or RHP preparation.

SEBI LODR Regulation 17 and Section 149 of the Companies Act require specific mixes of executive, non-executive, and independent directors, along with three mandatory board committees that must be constituted and functioning before the filing.

Companies that begin board composition work only at the DRHP stage are simultaneously running a board search, managing regulatory timelines, and absorbing the listing process – a compression that consistently produces rushed appointments and governance gaps that SEBI reviewers and institutional investors notice.

Table of Contents

A company is six months from filing its DRHP.

The investment banker has completed the initial governance review.

The finding: the board does not meet SEBI LODR (Listing Obligations and Disclosure Requirements) Regulation 17 requirements.

- The audit committee lacks the required independent majority.

- The nomination and remuneration committee has not been formally constituted.

- One person the promoter had assumed would serve as an independent director turns out to have a commercial relationship with a subsidiary that disqualifies their independence under the Act

The company now has four to five months to identify, assess, negotiate with, and formally appoint two or three independent directors – while simultaneously managing the investment banker, legal counsel, auditor, and merchant banker workstreams that a DRHP preparation requires.

The board search is now competing with every other critical IPO workstream -> investment bankers, legal counsel, auditors, regulatory filings, and due diligence-for the same limited window before DRHP filing.

This is not an unusual scenario. It is the default outcome for companies that treat board composition as a pre-IPO compliance checklist item rather than a governance capability that needs to be built well in advance of the listing.

This guide covers what pre-IPO governance requires, how the compliance-to-effectiveness hierarchy actually works, the five mistakes companies make most often in building their IPO board, the four director profiles that matter most, and how long the board search process realistically takes.

What the Regulations Actually Require and What They Mean in Practice

The regulatory framework for listed company board composition sits across two instruments: SEBI LODR Regulation 17 and Section 149 of the Companies Act 2013.

Rather than reproducing the text, what follows is what each requirement means for a company building its IPO board.

Board Composition Under Regulation 17

At least half the board must be non-executive directors.

If the chairperson is executive, or related to the promoter, at least half the board must be independent directors.

If the chairperson is a non-executive director unrelated to the promoter, at least one-third must be independent.

Every listed company must have at least one woman director.

Pipal Tree Insight : What This Means In Practice

Most founder-led pre-IPO companies have an executive chairperson or one closely connected to the promoter family.

That automatically triggers the 50% independence threshold.

For a six-member board - a common pre-IPO structure - that means three fully independent directors who meet both the letter and the spirit of the independence test.

Many promoters doing this count for the first time, discover they are two or three seats short.

The woman director requirement is not separate from this - she must also qualify as genuinely independent if the company is to meet both requirements simultaneously.

The Independence Test

An independent director must have no pecuniary relationship with the company beyond sitting fees, no managerial position or executive role, no material relationship with the promoter, and no shareholding above 2% (including relatives).

In May 2025, SEBI’s informal guidance in InfoBeans Technologies confirmed that independence is to be assessed holistically, not by narrow technical compliance with a negative list.

A part-time commercial relationship, or a consulting role in a subsidiary, can be enough to disqualify.

Pipal Tree Insight : What This Means In Practice

Independence is increasingly assessed by SEBI on substance, not form. A person who has worked with the company in any capacity, has a commercial relationship with a promoter-related entity, or has any financial arrangement beyond sitting fees is likely to fail the holistic independence test even if they pass the literal definition.This is why promoter-network candidates - the first instinct of most founders when building their IPO board - are structurally problematic. The people you know well are usually the people SEBI will question most.

The 3 Mandatory Committees

Audit Committee (Regulation 18)

Minimum three directors, at least two-thirds independent, chaired by an independent director.

The chairperson of the audit committee must be present at the AGM to answer shareholder queries.

At least one member must have financial and accounting knowledge.

Nomination and Remuneration Committee (Regulation 19)

Unlike the audit committee, the NRC is composed exclusively of non-executive directors – at least three, with a two-thirds independent majority, chaired by an independent director.

Its mandate in the context of an IPO preparation is particularly significant: the NRC is responsible for identifying, evaluating, and recommending board candidates, which means it structurally governs the very board-building exercise this guide describes.

A company without a functioning NRC cannot credibly claim to have run a rigorous director appointment process.

Stakeholder Relationship Committee (Regulation 20)

Required once the company has more than 1,000 shareholders at any point in the financial year. For most pre-IPO companies this triggers at or before the IPO itself.

Pipal Tree Insight : What This Means In Practice

SEBI reviewers and the company’s bankers will request committee meeting minutes as part of DRHP due diligence. Committees constituted three months before the filing, with no meaningful meeting record, are a visible governance gap. An audit committee that has not reviewed management accounts, engaged with internal audit findings, or challenged the CFO in any documented meeting is not a functioning committee - regardless of whether it appears in the governance section of the DRHP.

Board Composition vs Board Governance vs Board Effectiveness

These three concepts are often treated as the same thing. They are not, and understanding the hierarchy matters for building an IPO board that serves the company beyond the listing day.

| Level | What It Means |

| Compliance | The board meets the minimum requirements of Regulation 17 and Section 149. The right number of independent directors, the right committee structures on paper, the woman director appointed. |

| Governance | The board actually functions as intended. Committees meet regularly and deliberate genuinely. Independent directors review management accounts, challenge assumptions, and leave a paper trail that reflects real oversight – not rubber-stamping. |

| Board Effectiveness | The board adds strategic value beyond oversight. Directors bring expertise, relationships, and perspectives that the promoter team does not have. The board shapes strategy, not just approves it. |

Most pre-IPO companies achieve compliance.

A smaller number achieve governance.

Fewer still achieve board effectiveness.

SEBI’s review process focuses on compliance and governance – institutional investors, particularly FIIs and mutual funds evaluating the IPO book, extend that scrutiny to effectiveness.

The director appointment process determines which level you build toward. That is why board search matters.

Why Is Pre-IPO Board of Directors Composition Always Rushed?

Three patterns explain most of the IPO board of directors composition failures we see.

None of them involve bad intentions. All of them involve predictable miscalibration.

Conflating Compliance With Governance

When board composition is treated as a legal requirement to be met rather than a governance capability to be built, the natural instinct is to address it when it becomes a blocking issue – which is the DRHP stage.

A company secretary flags the Regulation 17 gap.

The management team adds it to the pre-IPO checklist.

By the time it gets addressed, the listing timeline is the constraint, not the board quality.

Underestimating The Board Search Timeline

Finding an independent director who is genuinely independent (not in the promoter’s network), brings relevant expertise, has available board capacity, and is willing to commit to a pre-IPO company takes significantly longer than most management teams expect.

The assessment, reference checking, independence verification, and formal appointment process is a minimum 12–16 week exercise per director – and that assumes the first candidate engaged accepts the role.

Assuming The Existing Network Is Sufficient

Many promoters believe that building an IPO board means activating their existing professional relationships.

This produces directors who are known, comfortable, and highly unlikely to provide the independent challenge that institutional investors and SEBI expect. The promoter’s network produces familiar faces. An IPO-ready board requires genuine independence – and the two are structurally in tension.

“Most founders come to us when the DRHP is six months away and the investment banker has flagged a board composition gap.

That conversation is not impossible, but it is always a compromise.

The board you build in three months under timeline pressure is a different board from the one you build in twelve months with the space to be selective.”

Five Common Mistakes Companies Make When Building Their IPO Board

Appointing Directors Too Late

The most expensive mistake, because its cost is invisible until the DRHP stage when the timeline is fixed and the options are limited.

A board search that begins 6 months before the target listing date starts with a compressed window that eliminates the best candidates – the ones who receive more than one approach, assess the company carefully, and take time to decide.

Late appointments produce whoever was available and willing, not whoever was right. The cost of getting this wrong in delayed listing, board dysfunction post-IPO, or a governance observation from SEBI – consistently exceeds the cost of beginning the process early.

Appointing Friends

The independence requirement is not satisfied by good intentions.

A director who has known the promoter for twenty years, attended the same business school, or has any commercial relationship with the company, its subsidiaries, or its promoter family fails the independence test on substance even if they technically pass a narrow reading of the definition.

SEBI’s May 2025 guidance on holistic independence assessment makes this more explicit than it has ever been.

The pre-IPO governance instinct to appoint trusted people is directly at odds with the listed company governance requirement to appoint independent ones.

A Board With No Listed Company Experience

Independent directors who have never sat on a listed company board before are discovering what listed company governance means at the same moment as the management team.

Neither side benefits.

The audit committee chair who has not previously managed the relationship between a board and its statutory auditors, or navigated a SEBI observation letter, is not equipped to guide the company through the first two years of listed company life.

At least one independent director on an IPO board should have prior listed company board experience – someone who has been through listing before and understands what the transition demands.

Inactive Committees

Committees constituted on paper but not functioning in practice are a material risk at the DRHP stage and a liability post-listing.

An audit committee that has not challenged a single line of management accounts, or a nomination committee that has never actually run a director identification exercise, cannot claim to be performing its governance role.

SEBI reviewers read committee minutes carefully. Institutional investors’ governance teams read them too.

A committee meeting record that shows unanimous approvals with no documented deliberation or challenge is not evidence of good governance – it is evidence of a committee that exists to satisfy a requirement, not to perform a function.

All Directors Appointed Simultaneously

With a maximum tenure of two five-year terms (ten years total) under the Companies Act 2013, a company that appoints three independent directors in the same month has built a board succession cliff.

In five years, all three will be due for re-appointment consideration at the same time. In ten years, all three will need to be replaced simultaneously.

Staggered tenures – planned deliberately at the time of initial appointment – create a board that renews itself progressively rather than episodically, providing continuity across leadership transitions.

What an IPO-Ready Board Actually Looks Like

A board of directors composition that meets Regulation 17 numerically but lacks genuine governance capability will satisfy the filing checklist and fail the institutional investor scrutiny that follows. The distinction between technical compliance and substantive readiness is what separates IPO boards that serve companies well from ones that create governance problems in the first year of listed company life.

Functional Independence

Independent directors who will actually challenge management - not simply approve recommendations. Institutional investors, FII managers, and proxy advisory firms like IiAS and Stakeholders Empowerment Services read board meeting minutes and ask specific questions about board deliberations during the book-building process. A listed company board where every resolution is unanimous and no dissent is ever documented raises questions about whether independent directors are functioning independently.

Relevant Expertise Coverage

The board collectively should cover financial literacy (audit committee requirement), sector or market expertise in the company’s domain, and the governance experience appropriate to a listed entity. A board composed entirely of promoter-family non-executives plus nominally independent external members rarely achieves this balance.

Active Committee Functioning

The audit committee in particular must be genuinely operational before the DRHP is filed - reviewing quarterly management accounts, engaging with the statutory auditor, and overseeing internal audit findings. The nomination committee must have a documented process for director identification, not just a post-facto approval mechanism.

Tenure Planning

With maximum ten-year independent director tenures, an IPO board needs to be designed with staggered appointments so that renewals happen progressively. This requires thinking about tenure distribution at the point of first appointment - a consideration that companies making simultaneous appointments under timeline pressure rarely have the space to address.

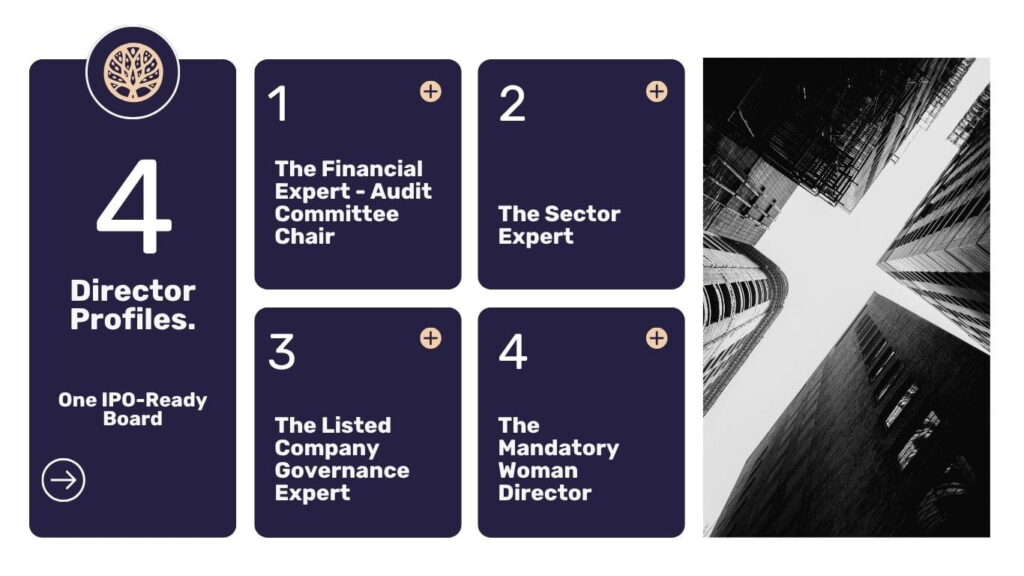

The 4 Director Profiles Pre-IPO Companies Need

Each profile is harder to find than it appears.

The specific independence requirements, the SEBI-mandated expertise thresholds, and the limited supply of candidates who have both the qualifications and the available board capacity make the pre-IPO board search a more specialised exercise than most promoters anticipate.

The Financial Expert - Audit Committee Chair

Requirements are specific: financial and accounting knowledge (more than basic literacy for an audit committee chair), genuinely independent, available to chair a listed company audit committee, and willing to engage substantively with the CFO and statutory auditors on a quarterly basis.

Retired CFOs and finance directors of listed companies are the natural candidate pool - but the best ones are already on multiple boards, and the seven-listed-entity cap under SEBI LODR means available capacity is a real constraint. A candidate who satisfies all the criteria but has no remaining listed company board capacity cannot take the role.

The Sector Expert

An independent director who brings genuine credibility in the company’s market - a former senior executive from an adjacent industry, a large customer base, or a relevant institutional context.

Finding someone with real sector expertise who also passes the independence test is harder in practice than in theory. India’s senior professional community is relatively small, and the candidate who knows the company’s market well often knows the promoter personally - which creates an independence question that disqualifies them. The search must go wider than the promoter’s own sector relationships.

The Listed Company Governance Expert

An independent director who has served on one or more listed company boards before and understands firsthand what SEBI, institutional investors, and proxy advisors expect from board governance.

This is the director who sets the tone for how the board operates as a listed entity - who understands the difference between the governance culture of a private company and a listed one, and who can help the management team make that transition credibly. At least one director of this type should sit on every IPO board.

The Mandatory Woman Director

SEBI’s requirement for at least one woman director, and the requirement for at least one independent woman director for the top 1000 listed entities, is a governance requirement, not a token one. Institutional investors and ESG evaluation frameworks examine whether the woman director holds a substantive role with genuine committee responsibilities.

Appointing a promoter family member who is nominally independent, or a person who satisfies the requirement on paper but attends meetings without meaningful participation, does not satisfy the governance expectation behind the rule. The search for this profile should be conducted with the same rigour as the other three.

How Long the Board Appointment Process Actually Takes

Planning backwards from the DRHP filing date requires understanding the realistic minimum timeline for a board search and appointment process. The following is the structure of a well-run independent director appointment exercise.

Pipal Tree Insight : The Planning Implication

12–16 weeks is the minimum for a well-run board search and appointment process for a single independent director. For two or three directors appointed in sequence or parallel, 18–24 weeks is a more realistic planning figure. A company filing its DRHP in six months does not have this window for board composition work. A company beginning the process 12–18 months before its targeted listing date does.

| Phase | What happens |

| Weeks 1–2 | Role definition – what expertise gaps does the board have, what does the ideal profile look like for each seat, what committee roles need filling, and what independence constraints apply? |

| Weeks 3–6 | Market mapping and candidate identification – who are the qualified, available, genuinely independent candidates? Not the promoter’s network, but the broader market of potential directors with the relevant profile. |

| Weeks 7–10 | Candidate conversations, independence verification, and reference checking. Independent directors assess the company as carefully as the company assesses them – the due diligence is bilateral. |

| Weeks 11–12 | Board resolution and formal appointment – DIN verification, letter of appointment, MCA filing, consent forms, and the proficiency self-assessment requirement under Section 150. |

| Weeks 13–16 | Induction, committee assignment, and first board meeting participation. A new independent director who has not been inducted properly is not prepared to fulfil their governance role. |

The Board Search Perspective

Board search is structurally different from executive search, and the difference matters for pre-IPO companies trying to build a genuinely strong IPO board.

The executive search process begins from a role that needs to be filled.

Board search begins from a governance gap that needs to be addressed – and the candidate pool is smaller, more self-selecting, and harder to access through conventional recruitment channels.

The strongest independent directors are rarely actively seeking board appointments.

They are identified through sector networks, prior board relationships, and long-term connections built across multiple mandates – which is why the earliest stage of a board search looks less like recruitment and more like relationship intelligence.

A specialist board search partner who has placed directors across listed company boards in your sector already has access to these relationships. A general recruiter working from a database does not.

Three things a specialist board search partner brings that a promoter’s own network cannot:

- Access beyond the promoter’s circle: The independence requirement makes promoter-network candidates structurally problematic. A search partner with no commercial relationship with the company can identify and approach candidates who meet the independence test by definition.

- Assessment beyond credentials: An independent director’s willingness to challenge management is not visible on a CV. It emerges from specific conversations about governance scenarios, how they have handled disagreements with management in previous board roles, and what their approach to audit committee oversight looks like in practice.

- Conflict navigation: Many otherwise qualified candidates have commercial relationships with the company, its competitors, or its promoters that create independence issues. An experienced board search partner identifies and navigates these before the approach is made.

The best independent directors are not on a list somewhere waiting to be approached. They are in the middle of two or three other board mandates, known to a small number of people who have worked with them directly over many years.

That is exactly why board search is not a recruitment exercise. It is a relationship exercise – and the relationship needs to exist before the need arises.”

Why Pipal Tree is one of the top executive search firms in India

→ 97% placement success rate across hundreds of leadership mandates.

→ 50+ years of combined search experience across our founding team.

→ 80% repeat engagement rate > our clients come back because our process works.

→ We combine the best practices of a global executive search firm with the entrepreneurial responsiveness and senior-partner involvement of a boutique consultancy.

How Pipal Tree Approaches Board Services

Pipal Tree’s Board Services practice is built on the same principles as this guide describes: finding directors with genuine independence and functional expertise, rather than recycling from a limited circuit of established board members. We look beyond the traditional director networks to identify candidates who bring fresh perspectives, complementary expertise, and the specific governance experience the company needs at its current stage.

We work with pre-IPO companies, PE-backed businesses approaching governance milestones, family businesses professionalising their boards, and listed companies refreshing director composition ahead of tenure completions.

For an overview of our approach to board succession and board advisory, our talent mapping guide covers the longer-horizon planning that board composition is a part of.

To discuss a specific board composition requirement, reach out at [email protected]

Frequently Asked Questions On Board Of Director Composition

Can a promoter’s family member serve as an independent director?

No. Section 149(6) of the Companies Act 2013 and Regulation 16(1)(b) of SEBI LODR both explicitly exclude relatives of promoters from qualifying as independent directors. The independence definition is not a judgement call on the relationship quality – it is a categorical exclusion. This applies to spouses, parents, siblings, and children of promoters.

How many independent directors should a pre-IPO company have before filing?

The minimum under Regulation 17 depends on the chairperson structure. For most founder-led companies with an executive chairperson or a chairperson related to the promoter family, at least 50% of the board must be independent directors. For a six-member board, that is three independent directors. It is prudent to have this composition in place and operating through at least two board meeting cycles before the DRHP is filed.

What happens if SEBI raises observations on board composition during DRHP review?

SEBI issues an observation letter specifying the required rectification and a timeline within which it must be addressed. In practice, this delays the listing timeline by weeks or months depending on the nature of the observation and how quickly the company can respond. A board composition observation – particularly one questioning the genuine independence of appointed directors – is among the more time-consuming to resolve because it requires identifying and appointing replacement directors before SEBI will clear the filing.

Does an independent director need to be SEBI-registered?

No formal SEBI registration is required. However, every person appointed as an independent director of a listed company must pass the online proficiency self-assessment test administered through the Indian Institute of Corporate Affairs under Section 150 of the Companies Act 2013. Directors who are already on the approved databank and have already passed the test are not required to repeat it, but new entrants to the independent director databank must complete it within one year of inclusion.

Is it possible to appoint additional independent directors after the IPO if needed?

Yes – but the context changes materially. Post-listing, any board appointment is subject to shareholder approval at the AGM or through a postal ballot, is reviewed by institutional investors and proxy advisory firms, and takes place under the scrutiny of a public company governance framework. Completing board composition before listing, with the space to make considered appointments, is structurally easier and produces better outcomes than correcting a governance gap under public company disclosure requirements.

These FAQs cover the most common questions we talk about board composition.

For a more broader questions on fees, timelines, and how the executive search process works, visit our Executive Search FAQ section.

If Your IPO Timeline Is 12–24 Months Away, the Board Conversation Starts Now

Board composition for a listed company is not a pre-filing checklist item.

It is a governance capability that takes 12–18 months to build properly – and the quality of the board you build in that window shapes the company’s listed company life far beyond the listing day itself.

If your company is on a 12–24 month IPO timeline and board composition has not been formally assessed against Regulation 17 and Section 149 requirements, the first step is understanding the gap: how many independent directors you need, what expertise profiles matter, and how much time a well-run search and appointment process realistically requires. We run that assessment as a preliminary conversation, with no engagement required.

Reach out at [email protected]

Sonia Sharma

"With over 25 years in talent leadership—including 20+ years in executive search—Sonia brings valuable dual perspective as Pipal Tree's founder. Her career spans both consultancy roles at prestigious firms (Korn/Ferry International, Accord India, Stanton Chase) and corporate leadership. Sonia specializes in executing confidential, high-stakes searches for global and Indian multinationals."