Every Indian family business reaches a moment when the person who helped build the financial foundation is no longer the person who can take it forward. This is not a capability story. It is a loyalty story with financial consequences. This article is for promoters, next-generation leaders, and boards navigating that moment — covering the signals that the transition has arrived, what professionalisation actually means in an Indian promoter-led context, the two non-negotiable filters for the right candidate, and how to manage the transition without losing what took two decades to build.

Table of Contents

A PE partner is sitting across from a third-generation promoter. The term sheet is on the table. There is one condition before the deal closes: a professional CFO in place within six months.

The promoter goes quiet.

They are thinking about Rajeev-ji

– 22 years with the business,

– Who joined the firm when he was 20 year old

– Who knows every account, every banking arrangement, every supplier.

– Who has never once taken a day off during year-end audit.

– Who is family, in every sense except blood.

What makes this different from any other CFO transition: this is not a capability gap to be closed with a hiring decision.

It is a relationship to be managed, an institution of one to be honoured, and a business to be protected through a change that is simultaneously operational and deeply personal.

Why This Transition to Family Businesses CFO Is No Longer an Exception

Across Indian business today, this transition is becoming a defining inflection point for an entire generation of family-owned enterprises simultaneously.

Four converging forces have made the question urgent for businesses that could previously postpone it indefinitely.

PE capital into mid-market India is at record levels.

Private equity and venture capital firms invested approximately USD 33 billion across 1,164 deals in 2025 (Venture Intelligence via Business Standard). Manufacturing PE deal value overtook healthcare in 2025, with significant deployment into family-owned mid-market businesses. Every PE investment triggers a governance conversation. That conversation almost always surfaces the CFO question within the first 100 days.

The second-generation succession wave is reshaping family business leadership.

India's first generation of post-liberalisation entrepreneurs is now handing the baton to children who studied abroad, think in systems, and want to build differently. According to Deloitte Private’s 2025 family business report, Indian family businesses are using technology adoption, governance reforms, and succession planning to mitigate risks - a structural shift towards professionalisation.

IPO aspirations have reached SME and mid-market businesses.

Between 2020 and 2024, over 600 SMEs listed on Indian exchanges, raising more than ₹20,000 crore collectively. The September 2025 SEBI IPO reforms tightened compliance and governance requirements, making the gap between a trusted finance head and an IPO-ready CFO impossible to bridge during the listing process itself.

Lender sophistication is reshaping debt-driven governance pressure.

NCDs, syndicated term loans, and credit ratings increasingly demand structured financial reporting, covenant compliance, and CFO-level accountability. The era of relationship-based corporate lending has contracted faster than most family businesses anticipated.

This article focuses on what these four forces actually require in finance leadership – and how to manage the transition without destroying what the outgoing finance head built. The Private Company CFO archetype in our Indian CFO Playbook defines what this role requires structurally.

This article covers what that framework doesn’t – the human dimension, the transition mechanics, the consequences of delay, and the two filters that determine whether the right candidate even takes your call.

The Trusted Finance Head - What This Role Actually Is

Before discussing how to transition to a family businesses CFO, it is worth being precise about what is being transitioned. The trusted finance head in an Indian family business is not just a senior employee. They are an institution of one, built across decades of personal trust.

What they typically are

- A CA or senior commerce professional who joined when the business was a fraction of its current size – often 15–25 years earlier

- The only person who truly understands the complete financial history, including transactions and arrangements that were never formally documented

- The promoter’s personal financial advisor – handling family property, personal tax, sometimes inter-family financial arrangements

- The custodian of banking relationships built on years of personal trust with specific branch managers, credit heads, and treasury teams

- The person who was in the room through IPO discussions that didn’t happen, banking crises that were quietly resolved, and family succession conversations that never left the building

What they are not (anymore) - and this is not a criticism

- Equipped to build investor-grade MIS, reporting packages, and financial dashboards from scratch

- Experienced in managing PE investor reporting requirements and fund covenant obligations

- Capable of building the finance team the business now requires beneath them

- Comfortable with the governance architecture that institutional capital demands

The core tension

1. Their institutional knowledge is irreplaceable.

2. Their capability ceiling is real.

The mistake is treating these two facts as reasons to either keep them indefinitely or dismiss them abruptly – when the right answer is a managed transition that honours the first while addressing the second.

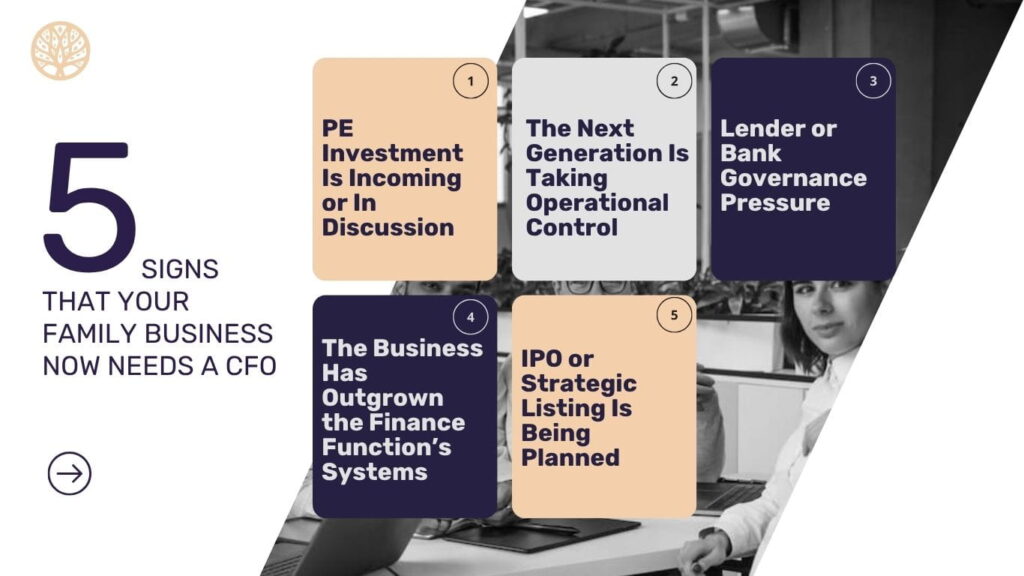

Five Signals That the Transition From Finance Head To Family Businesses CFO Has Arrived

Most promoters know they need to make this transition to a family businesses CFO before they make it.

What they are waiting for is the unambiguous signal that the moment has come.

The five signals below appear with consistency across the family businesses we have worked with through this journey.

PE Investment Is Incoming or In Discussion

PE firms and growth equity funds entering as investors almost universally require a professional CFO as a condition of or consequence of investment.

They need investor-grade reporting, fund covenant management, ESOP accounting, and communication in the language of EBITDA bridges and financial models.

The trusted finance head cannot deliver this, not because of capability, but because the role they have been performing is fundamentally different.

Search timing reality: PE investors set timelines.

A promoter who waits until after the investment closes to begin the CFO search typically has 90 days to complete a search that should take 16–24 weeks.

The Next Generation Is Taking Operational Control

When the founder’s son or daughter takes over as MD or CEO, they frequently find that the trusted finance head is an extension of the founder’s informal operating style – not equipped to support the systems-oriented leadership the next generation wants to build.

According to PwC’s 12th Global Family Business Survey Indian family businesses stand out globally for confidence and ambition – but the survey explicitly identifies the need for better governance structures and succession planning.

The next-gen transition is frequently when the finance professionalisation conversation becomes unavoidable.

Lender or Bank Governance Pressure

As family businesses grow and take on structured debt – NCDs, term loans, working capital lines, sometimes syndicated facilities – lenders impose financial covenants and reporting obligations that exceed the trusted finance head’s capability.

A credit rating exercise, a rights issue, or a bank syndication almost always surfaces the gap publicly.

The promoter discovers that the trusted finance head cannot manage the relationship with the credit rating agency or produce the financial projections the banker requires at the level expected.

The Business Has Outgrown the Finance Function’s Systems

Some businesses reach ₹500–1000 crore in revenue with:

– An ERP implemented five years ago that nobody fully uses,

– A finance team of eight people doing work that a well-designed system and four people could handle,

– And a monthly MIS that takes three weeks to produce.

The trusted finance head built what the business needed at ₹50 crore.

It was exactly right for that moment.

The business scaled.

The function never did.

IPO or Strategic Listing Is Contemplated

SEBI’s requirements for IPO-bound companies are uncompromising on financial governance. The September 2025 SEBI IPO reforms introduced sweeping changes to listing requirements, recalibrating the way companies prepare for and execute their listings which require finance leadership.

The IPO process itself will expose the gap, the question is whether the promoter addresses it before the DRHP or discovers it mid-preparation.

Many promoters approach SME IPO platform assuming it carries lighter governance requirements. That assumption no longer holds. Following SEBI’s 208th Board meeting, governance-ready financial statements, clean related-party transaction documentation, and audit committee-ready reporting are no longer optional even on the SME route.

The trusted finance head who has not built these foundations will be exposed during merchant banker due diligence – often before the DRHP is even filed.

The promoter who discovers this mid-process faces the worst possible outcome: they have committed publicly, engaged the merchant banker, and are on a visible timeline. Finding and onboarding a new CFO at that stage is not just disruptive – it can delay or derail the listing entirely.

What Happens When the Transition Is Delayed Too Long

You may have come across articles on family business CFO transition which stop at “why it should happen.”

Few discuss what actually breaks when it doesn’t happen on time.

The consequences below are not hypothetical – they are patterns we have seen play out across Indian family businesses that postponed the decision past the point of healthy choice.

Investor distrust

PE investors or board members who observe that the finance function is inadequate start questioning the promoter’s judgment more broadly. The finance leadership gap becomes a governance credibility signal, not just an operational one. The cost is not the next investor conversation - it is the conversations that don’t happen because the word has quietly spread.

Lender escalation

A missed reporting covenant, a delayed financial statement, or an inadequate response to a credit agency query can trigger loan recall conversations. These escalations happen faster than promoters expect once lenders have lost confidence in the finance function. The cost of restoring lender confidence after it has been lost is significantly higher than the cost of preventing the loss.

Finance-team attrition

The best people in the finance function below the trusted finance head - the ones the professional CFO will eventually need as the nucleus of a new team - are often the first to recognise the ceiling. They leave for companies where the finance function has room to build. What remains is the team that couldn’t leave. By the time the new CFO arrives, the rebuild is harder than it needed to be.

Reporting opacity and founder dependency risk

When the entire financial intelligence of the business lives in one person’s memory, the business has a single point of failure. The trusted finance head’s absence - whether through illness, departure, or unforeseen event - can paralyse reporting, banking, and compliance functions simultaneously. This is not a hypothetical risk for businesses of a certain age and scale. It is a calculable one.

Stalled transformation initiatives

ERP upgrades, digital finance transformation, new product line P&L visibility, cost accounting redesign - every major finance infrastructure investment is constrained by the capability ceiling of the person leading the function. The business plans the transformation. The function cannot execute it. The investment is made; the value is not realised.

Failed IPO or investment timelines

The cost of discovering the finance function gap during DRHP preparation, PE due diligence, or a credit rating exercise is not just financial. It is reputational. And it is always more expensive than addressing it proactively. The market remembers the listing that was withdrawn, the investment that fell through, the credit rating that was downgraded - long after the underlying cause has been corrected.

The Trusted Finance Head vs the Professional CFO

The distinction between these two roles is not about seniority or credential – it is about what each role was designed to do, and what the business needs at different stages of its growth. The table below is not a ranking. Both profiles have served the business well in their moment. The question is which profile the business needs for its next chapter.

| Dimension | Trusted Finance Head | Professional CFO |

| Core value | Loyalty and continuity | Scalability and governance |

| Reporting style | Relationship-based | System-based |

| Primary strength | Institutional memory | Financial architecture |

| Team model | Loyalty-driven | Capability-driven |

| External interface | Banks, auditors, tax officers | PE investors, boards, rating agencies |

| Financial history depth | Deep – 15–25 years of context | Limited at entry, built over time |

| System-building capability | Low – built for current scale | High – designed to build the next scale |

| Risk profile | Scalability ceiling | Cultural mismatch and pace miscalibration |

| Replacement risk | Single point of failure | Manageable – function outlives the person |

The Important Note

Neither column is a criticism.

The trusted finance head is exactly right for the business they helped build. The professional CFO is exactly right for the business the promoter is trying to create. The table defines the transition, not the verdict.

What “Professionalisation” Actually Means in an Indian Promoter-Led Context

This is the word that creates the most anxiety for promoters – because it is consistently understood as “losing control” when it actually means “gaining visibility and building systems that don’t depend on one person’s memory.”

What it is NOT

- Replacing loyalty with process

- Bringing in someone who doesn’t understand the promoter’s context or vision

- Surrendering financial decision-making to a hired hand

- Being forced to change how the promoter thinks about the business

What it IS, specifically

Building investor-grade financial infrastructure.

Monthly MIS that takes days, not weeks. P&L by business unit, not just consolidated. Working capital dashboards. Cash flow forecasting that is actually used for forward decisions rather than backward reporting.

Creating governance structures that survive the promoter.

Related-party transaction policies. Audit committee-ready reporting. Board-level financial communication that external directors can engage with substantively.

Separating personal and business finances.

One of the most emotionally charged dimensions of professionalisation in Indian family businesses. Many promoter-led businesses have genuinely intertwined personal and business financial flows accumulated over decades of the business being an extension of the family. The professional CFO must manage this with discretion and patience - not disruption.

Building a finance team beneath the CFO.

The trusted finance head typically built loyalty-based teams. The professional CFO builds capability-based teams. This structural change - who reports to whom, what skills are valued, what the performance standard is - is a significant internal culture shift that requires active management.

“The promoters who fear professionalisation most are the ones who discover, twelve months later, that they had been operating semi-blind. The professional CFO doesn’t take financial control away from the promoter.

They give the promoter better financial control than they have ever had – through real-time visibility and systems that don’t break when one person is unavailable”

How to Manage the Transition From a Trusted Finance Head to a Family Business CFO

The Knowledge Transfer Window (3–6 months, non-negotiable)

The overlap period between outgoing and incoming finance leadership is not a courtesy.

It is the most valuable investment in the transition. What must be formally extracted and documented before the trusted finance head exits:

- Banking relationships – not account numbers but the personal relationships with branch managers, credit heads, and treasury teams built over years

- Tax history and open positions – pending assessments, informal understandings, long-standing interpretations of grey-area provisions

- Supplier and customer credit arrangements – many are entirely informal and exist only in the outgoing person’s memory

- The context behind balance sheet positions – the history that no audit file explains

The Promoter’s Active Role

The promoter cannot be a passive observer during this transition.

They must actively bridge the two people – introducing the incoming CFO into banking relationships personally, validating the outgoing person’s institutional knowledge in the new CFO’s presence, and making the handover a signal of respect rather than replacement.

3 Paths for the Outgoing Finance Head

Path 1: Advisory or consulting role.

Retained on a part-time or project basis for 12–24 months. Particularly valuable for tax matters with long history, regulatory filings, and banking relationships that need continuity beyond the handover period.

Path 2: Lateral move within the organisation.

Moves to Head of Accounts, GM Finance, or a senior administrative leadership role beneath the new CFO.

Works only when both parties genuinely accept the new dynamic – forced acceptance creates political friction that undermines the new CFO’s authority within weeks.

Path 3: Dignified exit

The Pipal Tree Insight: The Moment That Defines the Culture

How the promoter handles this transition is watched by every employee in the organisation.

A poorly managed exit – where the trusted person feels discarded after decades of service – sends a signal about how loyalty is valued that no subsequent HR policy can reverse.

A well-managed transition becomes a cultural reference point for the professionalised business the promoter is trying to build.

Why Some Professional CFO Hires Fail Within 18 Months

Pattern 1: The promoter wanted visibility without accountability

The CFO was hired to build systems, but every decision still required the promoter’s personal approval. The CFO could not act on the analysis they produced. The reporting got better. The decision-making didn’t change. Within 18 months, the CFO left for a mandate where their authority matched their responsibility.

Pattern 2: The CFO tried imposing MNC systems at MNC speed

A professional CFO from a large corporate environment arrived with a 90-day transformation plan. They tried to implement in six months what the organisation needed 24 months to absorb. The resistance they created became permanent opposition. The promoter eventually sided with the organisation. The CFO’s technical recommendations were correct. Their pace was wrong.

Pattern 3: The outgoing finance head was not managed through the transition

Nobody told the outgoing leader what their role was during the handover period. They interpreted the ambiguity as a mandate to protect their position. Quietly, methodically, they undermined the new CFO’s access to information, banking relationships, and team loyalty. The new CFO resigned. The original structure reasserted itself.

Pattern 4: No knowledge-transfer period

The new CFO arrived to a financial black box. Six months in, they were still discovering arrangements, positions, and relationships that had no documentation. The promoter grew impatient with what felt like slow progress. The CFO grew frustrated with what felt like organisational obstruction. Both were right.

Pattern 5: Misaligned expectations about mandate

The CFO was told they would build a professional finance function. They discovered the promoter’s definition of “professional” meant “better reports for the same decisions made the same way.” The mandate was narrower than promised. Trust eroded on both sides. The CFO exited.

The Right Profile For A Family Business CFO: The Two Non-Negotiable Filters

Across the family business CFO searches we have run, two filters appear with consistency in what promoters actually look for – often unconsciously – in candidates. These filters are rarely articulated in job descriptions but consistently determine which candidates make it through final interviews and which do not.

Filter 1: Stability as a Proxy for Trustworthiness

In a 30-year career, no more than 2–3 job changes. Current role must show a minimum of 5+ years of tenure.

This is not a conservative preference - it is a deeply psychological filter. A promoter who has worked alongside the same finance person for two decades has an implicit model of professional loyalty: someone who stayed through difficult years, who did not leave when a better offer came, who chose the relationship over the opportunity.When evaluating a new CFO, they are unconsciously pattern-matching against that model.

A candidate with 30 years of experience and 7–8 job changes - regardless of the quality of each transition - reads as someone who optimises for personal career progression over organisational commitment.

That signal, however unfair to the candidate, disqualifies them in the promoter’s evaluation before the second meeting.The Search Implication

The right candidate is almost never actively looking.

They are 5+ years into a stable role at a company they are genuinely committed to. They are not on job boards. Reaching them requires targeted, relationship-based outreach from a search partner who has earned the credibility to represent an opportunity to a deeply settled professional.

As we discuss in our guide on executive search versus recruitment, this is a headhunting search by definition – not a recruitment exercise.

Filter 2: Must Have Worked With Promoters - Ideally One Who Has Already Made This Journey

The right candidate has not merely worked in a private company :

- they have worked in close proximity to a promoter who went through professionalisation and came out the other side.

- They have sat in the room when the PE investor asked uncomfortable questions.

- They have helped separate personal and business finances.

- They have managed the anxiety of the first proper audit and the first board-level financial presentation to external directors.

This experience cannot be transferred from a textbook or developed in a corporate career. It is earned in the room, over the years, at the side of a promoter navigating the journey the incoming promoter now faces.

Where to find these candidates:They are not in large MNCs or listed corporate finance functions. They are in other promoter-led Indian businesses that have already completed some version of this journey - family businesses that have taken PE investment and built governance post-investment, businesses that professionalised ahead of a listing, industrial conglomerates that brought in professional management in the last decade. The candidate pool is finite, specific, and requires genuine market mapping to access.

Why Pipal Tree is one of the top executive search firms in India

→ 97% placement success rate across hundreds of leadership mandates.

→ 50+ years of combined search experience across our founding team.

→ 80% repeat engagement rate > our clients come back because our process works.

→ We combine the best practices of a global executive search firm with the entrepreneurial responsiveness and senior-partner involvement of a boutique consultancy.

In Practice : Three Transition Patterns

-

Pattern 1: The PE-Entry Trigger

Context: A glass manufacturing company receives PE investment. The investor’s governance requirements include CFO-level financial reporting within the first operating year. The existing VP Finance is technically strong but not equipped for investor reporting cadence or board-level communication.

Approach: Professional CFO hired from another PE-backed industrial company - 7 years of tenure in current role, previously worked with a promoter-led manufacturer that had completed a PE governance upgrade. Existing finance head repositioned as Head of Accounts reporting to the new CFO. 6-month structured knowledge transfer.

Outcome: Both leaders stay. PE investor gets the governance upgrade. Business retains the institutional knowledge.

-

Pattern 2: The Next-Generation Transition

Context: A multi-business textile manufacturer navigates leadership transition from founder to second generation. The new MD wants to build a professional management layer across functions. The Group CFO appointment is the first senior external professional hire at the leadership level.

Approach: Candidate profile: 28 years of experience, 3 jobs, current role 6 years, previously served as CFO of a listed non-textile company that had professionalised from a promoter-led base. The trusted finance head of the founding generation becomes the new CFO’s formal knowledge transfer partner for 9 months.

Outcome: Roles clearly defined. Outgoing finance head exits on his own terms, with full honours, on a timeline he chose.

-

Pattern 3: The Scale Trigger

Context: A composite manufacturing company has grown 3x in five years. The company had big plans with mult-plant setup. The finance function has not kept pace. Cost accounting is rudimentary. MIS is unreliable.

Approach: CEO and CHRO search followed immediately by a finance leadership build-out. The trusted finance head exits with full dignity after a 6-month transition - a genuinely respected departure, handled personally by the promoter.

Outcome: A cultural reference point for the business the new leadership team is building. The exit itself becomes a statement of values.

How Pipal Tree Approaches This

Our work with family businesses navigating this transition is built on a specific understanding: this is not a standard CFO search.

The human dimensions require as much attention as the functional requirements.

- Our process starts with understanding the outgoing leader and what they represent – before defining what the incoming leader must be

- We help promoters think through the transition structure, not just the candidate profile

- We apply both filters – stability and promoter-proximity – as primary evaluation criteria, not secondary ones

- We assess for cultural fit and relationship capability as rigorously as we assess for financial competence

For the broader framework on CFO archetypes and how the Private Company CFO fits into the wider Indian executive landscape, see our Indian CFO Playbook.

For our dedicated practice on CFO search across archetypes, visit our CFO Search service page.

Frequently Asked Questions On Indian Family Businesses CFO Search

Should we tell the current finance head we are searching for their replacement?

This depends on which transition path is being taken.

If the outgoing leader will stay in an advisory or lateral role, early and direct conversation is almost always better – their participation in shaping the new role increases the probability of a smooth handover.

If the exit is clean, timing matters: the conversation should happen before the search becomes visible internally, but not so early that the outgoing leader becomes disengaged during the search period.

Can the existing finance head be developed into the professional CFO role with the right support?

Occasionally yes, more often no.

The capability gap is frequently less about technical skills (which can be developed) and more about the mental model of what the finance function is for (which is harder to change after 20 years of operating in a different model).

The honest assessment requires evaluating not just current capability but the willingness and capacity to operate as a fundamentally different kind of leader.

If the trusted finance head genuinely wants to make this transition and the promoter is willing to invest 18–24 months in coaching and support, it can work. The success rate is meaningfully below 50%.

How long does a family business CFO search in India typically take?

The honest answer: 16–24 weeks.

The stability filter the promoter demands is the same quality that makes the right candidate difficult to move. Promoters who expect a 60-day turnaround consistently compromise on the filters that matter most. This is not a search process failure – it is a direct consequence of selecting for stability.

How long should the knowledge transfer overlap period be?

Minimum 3 months, ideally 6 months.

The single most common structural failure in these transitions is shortening or eliminating the overlap under cost or time pressure. The cost of 3–6 months of dual finance leadership is significantly lower than the cost of a new CFO discovering, six months in, that they are missing context the outgoing leader could have provided in a single afternoon.

Why compensation alone rarely attracts the right CFO into promoter-led businesses

This is the insight most promoters resist initially. The right candidates – 5+ years in their current role, previously worked with promoters, proven track record of building governance – already have competitive compensation. They are not looking. A higher salary does not prompt them to consider a move.

What prompts consideration is:

– the quality and seriousness of the promoter,

– the clarity of the mandate,

– the credibility of the transition structure being offered, and

– the assurance that they will be given genuine authority to build.

This is why recruitment exercises – posting a job description, engaging multiple agencies – consistently fail for this search.

The right candidate is not waiting to be found.

They need to be engaged through a conversation that begins with the opportunity’s strategic context, not its compensation package. See our broader piece on why top executives decline job offers for the full pattern.

How do we retain a professional CFO in a family business environment once they’re in place?

The single most important retention factor: delivering on the mandate clarity that was offered during the search.

The professional CFOs who leave within 18 months almost always cite one of two reasons – either the promoter reclaimed the authority they had promised to delegate, or the knowledge transfer from the outgoing leader was inadequate and they spent their first year discovering rather than building.

The retention question is determined by promises kept, not perks added.

These FAQs cover the most common questions we hear from promoters when doing a CFO search for them.

For a more broader questions on fees, timelines, and how the executive search process works, visit our Executive Search FAQ section.

If You Are Evaluating Whether Your Business Has Reached This Transition Point

This is one of the most consequential leadership decisions an Indian family business will make.

It is also one of the most personal.

Done well, the transition preserves what the trusted finance head built while creating the financial architecture the business needs for what comes next.

Done poorly, it damages both – and the cost is measured in years, not quarters.

At Pipal Tree Services, our conversations with promoters and family business leaders considering this transition are exploratory by design. They are diagnostic conversations, not pitch calls.

We help promoters think through three questions:

- Question 1: Has the business reached the transition point? If yes, which of the five signals is the dominant trigger?

- Question 2:What does the right transition structure look like for this specific business? Which of the three paths for the outgoing leader best fits the relationship and the business need?

- Question 3: What does the candidate market actually look like? How long will the search realistically take, and what will it require to move the right person?

If you are a promoter, board member, or family business leader navigating this question, we would welcome the conversation. Reach out to me at [email protected].

We can help define the mandate before the search begins. Because in a $2.4 trillion market, the most expensive mistake is not a bad quarter — it’s the wrong leader.

Sonia Sharma

"With over 25 years in talent leadership, including 20+ years in executive search. Sonia brings valuable dual perspective as Pipal Tree's CEO & founder. Her career spans both consultancy roles at prestigious firms (Korn/Ferry International, Accord India, Stanton Chase) and corporate leadership. Sonia specializes in executing confidential, high-stakes searches for global and Indian multinationals."